Mongolia: Why And How To Invest In China's Canada

Risks to Mongolia’s Growth

In Mongolia’s capital city of Ulan Bator, real estate investors believe developed property prices are rising 3 to 5% per month, and undeveloped land prices are rising 5 to 10% per month. Marc Faber has called Mongolia, “the Saudi Arabia of Asia,” for its vast wealth of natural resources in coal, copper, gold, and more. In a recent Bloomberg interview, real estate investor Sam Zell stated that Mongolia is the best economy to invest in for the next 5 to 10 years.

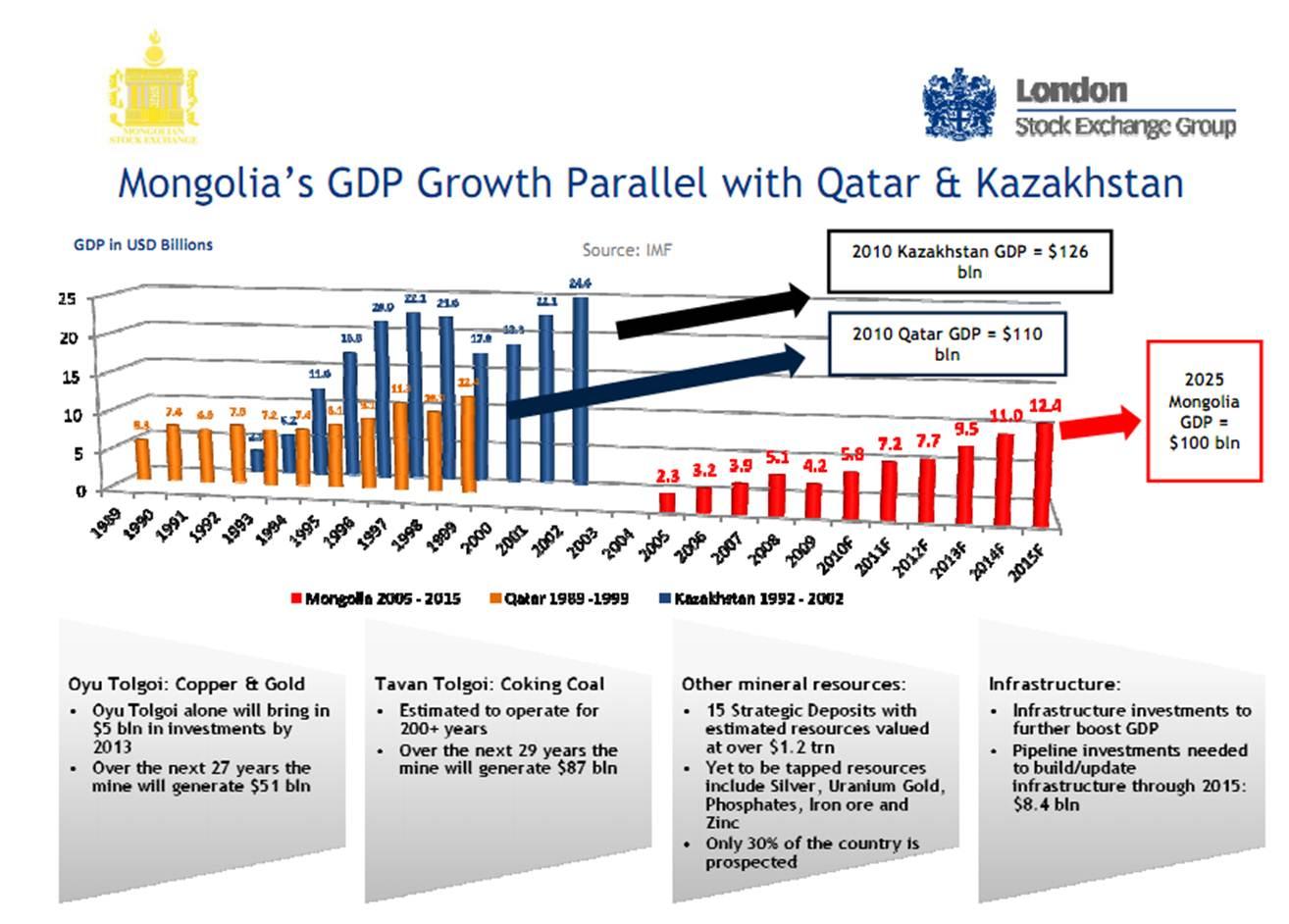

Mongolia’s potential is similar to the recent natural resource booms in Qatar and Kazakhstan, where there are stories of 30-fold increases in assets. The Mongolian government hopes to replicate the national resource boom successes in Chile and Norway. The goal is to avoid the resource boom problems taking place in Nigeria or Zimbabwe. The most optimistic think Mongolia is to China as Canada is to the U.S., a large geographic neighbor to the north of an industrial powerhouse, a country with large natural resource deposits and a small population north of a trade partner with limitless need.

(click image above to enlarge it)

Whether you want to invest $5,000 or $5 million, there are many ways for you to invest in Mongolia. The first thing to understand though is why Mongolia is at an investable moment now. After discussing Mongolia’s history, tax consequences, currency risk, and an assessment of investment risk will be addressed (scroll down to the header "Tax Consequences" if you are not interested in the history). In the following articles, equity investment, real estate investment, and investing in the Mongolia Stock Exchange through local brokers will be discussed. This series will conclude with a fifth article on the role of aid agencies in Mongolia's boom, and the potential outcomes of Mongolia’s economic boom for its people and its investors. How did Mongolia get here?

To understand Mongolia today, one has to understand Mongolia’s at times hostile and at times symbiotic relationship with China. Understanding this relationship explains the need for Mongolia’s other geographic neighbor Russia to serve as ballast against the influence of China over Mongolia. More than 80% of Mongolia’s exports go to China while about 90% of Mongolia’s petroleum comes from Russia. Landlocked, almost any good imported or exported passes through one of these two neighbors. Mongolia, sandwiched between these two powerful neighbors uses these two countries as geopolitical counterweights. Today, Russia balances a Chinese focus. While there is historical enmity with China, Mongolia’s natural resource boom depends clearly on China’s demand for natural resources.

Early History

Chinggis Khaan (1162 – 1227) established the great Mongol empire, the largest contiguous empire in the history of mankind. His iconic images that were banned during communism now rule state statues, tourist shops and history books of the country. Chinggis’ grandson Kublai Khaan (1215 – 1294) began the Chinese Yuan dynasty that lasted from 1271 to 1368.

The Chinese-led Ming Dynasty (1368 to 1644) displaced the Mongol-led Yuan Dynasty. For Mongols, this was difficult as it was the first time in two centuries that they only had access to resources within Mongolia.

Mongols and Manchurians united in the 1500s and managed to take over China to form the Qing Dyansty in 1644 that lasted until 1911 when the separate republics of China and Mongolia formed.

During over 250 years of rule, the Qing Dynasty transitioned from holding the Mongols in favor to holding greater favor toward its Chinese base population. This left Mongols to be a provincial sub-class of people.

The Qing Dyansty collapse was not orderly. The Republic of China still claimed reign over Mongolia although a 1915 treaty gave the Mongols some autonomy.

This early history and rivalry is still alive in Mongolia. A part of China today is “Inner Mongolia” where there is a significant Mongolian minority living under Chinese rule. Mongolia, the country, is a separate sovereign entity north of China’s “Inner Mongolia.” There are unproven urban legends of “white men” roaming the Gobi desert buying coal from Mongolian miners that refuse to do business with the Chinese and selling the coal onto the Chinese at a 10% profit. Like any urban legend, these rumors of Mongolians that refuse to do business with the Chinese has a basis in the country's subconscious. There is Mongol pride in Chinggis Khan and his empire, and a long history of resentment – and battle – with their southern neighbor that is today’s global economic empire, the country upon which their own economic boom depends.

Communism, poor utilization of assets and poor development of infrastructure

During World War I and the Russian Revolution of 1917,a series of armies (including Mongolia’s, the Chinese and the White Russians) attempted to strategically control Mongolia. When in July 1921,the Mongolian General Damdin Sukhbaatar with Bolshevik troops took control over today’s capital city Ulan Bator, Mongolia became the second communist country in the world. It remained under the communist influence until 1990.

In the mid-1930s, the Soviets, unhappy with the organization of Ulan Bator, tore most of the city down. The only pre-1930s structures in Ulan Bator today are a handful of temples. Thus, in the city of Ulan Bator, one can see from an aerial view a typical communist layout with a big square (Sukhbaatar Square); a horseshoe network of roads and buildings around the square; and in the west of the city, there are apartments that were constructed to spell out “USSR” in Cyrillic.

Communist Mongolia only developed that which it needed to. Most roads in Mongolia today are still dirt roads. Where there is hot water, such as in Ulan Bator, it is heated centrally at a plant, the communist way. As with many things centrally planned during the communist era, the hot water functions a bit more than half the time.

There are a number of mines in operation in Mongolia today that have operated since the communist era. However, the Soviets had their own wealth of natural resources so Mongolia’s resources, including a lot of coal that can be accessed by open pit mining, was left undeveloped. In communist times, there was no need to tap resources further.

Post-communism, a transition without funding

As communism fell in the Soviet Union, democracy took hold in Mongolia. The communist ruling Mongolia People’s Party (MPP), until recently known as Mongolia People’s Revolutionary Party (MPRP), continued to exist after communism as an evolving political party that is now only a distant cousin of its communist origins. The MPP and the Democrat Party have traded election victories since 1996 and recent elections between the two have been so close as to result in grand coalition power-sharing between the two.

The Soviets largely subsidized the Mongolian nation during the communist era. When the Soviets pulled out of the country, they took with them machinery and equipment, engineers and skilled laborers. The end of Soviet subsidies and investment was an economic train wreck.

During the 1990s, while former communist nations in Central and Eastern Europe received a lot of investment and attention, Mongolia suffered. There was no money to maintain existing infrastructure let alone develop new infrastructure.

Rules that discouraged mining investing

In 1997, new laws came on line that could encourage development of the mining industry in Mongolia. However, the 2006 Windfall Profit Tax of 68% on the mining industry caused most mining companies to pull up stakes on any further capital expenditures in the country.

The 2008 hiccup

The replacement for Soviet subsidies was not a self-sufficient government. Rather, Mongolia receives aid and development funds from many agencies. Aid agencies from the U.S., Korea, Japan, China, Switzerland, the European Bank for Reconstruction and Development, the World Bank, the International Monetary Fund, the United Nations, and more all have a presence and stakes in Mongolia.

Following the financial crisis’s knock-on effect in 2008, the year 2009 was harsh for Mongolia. The departure of mining companies after the Windfall Profit Tax of 2006 plus a global economic pull back was felt harshly in Mongolia. These events gave the two larger parties in the country an impetus to change policies toward mining companies again.

Mongolia today, laissez-faire to encourage mining investing

On January 1, 2010, the windfall mining tax was repealed and a new era in mining in Mongolia opened up. Around the same time, the government signed a deal with Ivanhoe Mines and Rio Tinto for them to jointly develop the world’s largest undeveloped copper-gold mine, Oyu Tolgoi.

While Mongolia has significant deposits of many resources including copper and gold, its largest natural resource is coal. Mongolia recently overtook Australia as the leading exporter of coking coal to China. Mongolia's Tavan Tolgoi coal deposit is the second largest coal deposit in the world, yet the effect of Tavan Tolgoi and the rest of Mongolia's mineral wealth on the economy are currently overshadowed by Oyu Tolgoi.

The IMF noted in June 2010 (on page 5 of the linked report), “The outlook for real GDP growth is dominated by the Oyu Tolgoi mine. The scaling up of mining will increase mineral GDP and will have significant second-round effects on other sectors… Once production from the Oyu Tolgoi mine starts in 2013, it will boost growth to over 25 percent. Real GDP growth is expected to average 10 percent over the medium term (2014–20)”

Estimates for the required capital expenditures to get Oyu Tolgoi into production now exceed $6 billion and the mine is expected to begin production in the second half of 2012. Using prices of $850/oz of gold, $14/oz of silver, and $2 per pound of copper, Oyu Tolgoi will produce an estimated $3 billion per year at full production during its first 10 years. Publicized analysis of the production typically uses these lower commodity prices. Current commodity prices will yield over $6 billion in production. The government maintains a 34% stake in Oyu Tolgoi in partnership with Ivanhoe and Rio Tinto.

Consider what this one mine changes. Mongolia’s population today is estimated to be between 2.7 and 3.1 million people. Many people still live nomadically while approximately 40% of the population lives in Ulan Bator. The World Bank has Mongolia’s 2008 GDP at $5.3 billion. The U.S. State Department estimated Mongolia 2010 GDP at $6.8 billion. The August 2011 World Bank Quarterly Report on Mongolia has 2010 GDP growing at 6.4% while the 2nd quarter of 2011 experienced GDP growth of 17.3% year over year. Reviewing the numbers from Oyu Tolgoi, its easy to see how one giant copper-gold mine – one of many mines coming online in the next few years – is by itself changing the economy.

Chinese demand and Mongolian production in perspective

This year, Mongolia passed Australia as the leading exporter of coal to China. Estimates are that Mongolia will export about 20 million metric tons of coal to China this year, and that by 2015, that number could rise to 30 to 50 million metric tons of coal. Estimates are that China is producing more than 3.5 billion metric tons of coal and still importing more than 100 million metric tons. China’s need for coal is growing. Mongolia cannot fully meet those needs. China can use all the coal that Mongolia will produce.

China has announced it has 1.9 million metric tons of copper inventories, which is about three months of their usage at this time. These are state owned strategic reserves similar to the United States government’s oil reserves. China used 6.8 million metric tons of copper in 2010. Oyu Tolgoi has been estimated to have up to 37 million metric tons of copper which will take a minimum of 40 years to get out of the ground once production commences. Again, Mongolia cannot meet Chinese demand based on these numbers, but if Chinese demand continues on the trajectory it has been, Chinese demand may be sufficient to purchase all the copper Mongolia can produce.

Tax consequences

Taxes are the same for foreigners and locals

The system as it stands taxes foreigners and locals at the same tax rates. Income taxes are 10% below 3 billion Togrog ($2.35 million) and 25% above that break point (this includes rental income). There is a capital gains tax of 10%. The tax on dividends is also 10%.

Double taxation with your home country

Some countries have a relationship with Mongolia that avoids double taxation, such as Canada. For citizens of other countries, including the United States, be advised that investments in Mongolia are currently subject to double taxation.

The exit tax – will it apply to your equity investments?

There is currently a 20% tax on profits when your funds leave the country. For investments in private equity vehicles, figuring out if this tax will impact you is a question to ask.

Real Estate taxes

If you purchase property in Mongolia individually, there will be a few additional taxes. There is a transfer stamp duty tax of 2% and property taxes currently run at 6/10 of 1%. Real estate taxes are no different for foreigners than locals.

Tax filing

If you invest in property in Mongolia, or open a bank account or brokerage account in Mongolia, you will need to file taxes in Mongolia. I am not an accountant, all tax information should be checked with licensed tax professionals in your home country and Mongolia.

Togrog

Mongolia’s currency is the Togrog. In the last 5 years, its trading range against the U.S. dollar has been 1,142 Togrog for $1 (October 27, 2008) to 1,642.60 Togrog for $1 (March 16, 2009). Since November 2010, it has stayed in a trading range between 1,200 and 1,315 Togrog for $1. For stability of the economy, the Central Bank of Mongolia is trying to keep the Togrog’s valuation steady. However, a surge in the mining industry will likely make appreciation in the value of the Togrog inevitable.

The August 2011 World Bank Quarterly Report has year over year inflation at 11.4%. The central bank of Mongolia raised rates to 12.25% in October. Inflationary pressures are real with the government planning to raise salaries for all state employees 53% next year according to an October 3, 2011, report.

Risks to Mongolia’s Growth

China’s changing needs

The World Bank quarterly update on Mongolia for August 2011 states, “China is the sole destination for Mongolia’s coal exports.” I believe this is a slight exaggeration as Prophecy Coal is known to be doing trial shipments to Russia. However, upwards of 80% of Mongolia’s exports go to resource needy China and any blips in China’s economy will be felt in Mongolia. While Mongolia’s massive coal deposits, as well as the fact that in three years Mongolia should account for 10% of global copper production, are mentioned persistently at meetings detailing Mongolia’s coming economic boom, Mongolia is geographically reliant on both China and Russia as import and export partners. Even if Mongolia can export to markets beyond China and Russia, their natural resource products will have to transport through China or Russia to arrive at any other countries (whereas other products from meat to cashmere can be transported by plane around the world; however these are not the products that will be the cause of an economic boom in the country). Thus, to a large extent, Mongolia is a leveraged play on China’s continuing growth.

Global recession and aid agency reliance

Until Mongolia’s mining industry ramps up significantly from current levels and infrastructure builds up greatly from current levels, Mongolia is still reliant on international aid agencies (the U.N. Development Program, World Bank, U.S. AID, Asia Development Bank, European Bank of Reconstruction and Development, et cetera). Mongolia is close to turning a corner on its economic development, but it requires stable and reliable funding to arrive at its destination. Global recession reducing aid agency funding could cause the Mongolian economy to stall.

Infrastructure

Infrastructure in Mongolia needs massive development and better planning. In Ulan Bator, residential areas continue to expand on the edges of town, but regardless of whether they are the poorer ger districts or luxury housing, people still have to go the center of town for shopping, schools, and hospitals, as the basic needs of life are not planned for when housing development land is sold. Luxury homebuilders and people working for NGOs in the ger districts concur on the flaws of Ulan Bator’s infrastructure development.

There is a new power facility being built in Ulan Bator that hopefully will relieve the pressure on the two existing power facilities. Currently, power outages for a couple of hours on any given day are an accepted part of life. Moreover, better urban planning for roads, hospitals, shopping areas, schools, plumbing, hot water, green spaces, and so on is needed. Buildings are being built with no street access. National parks have become built up residential communities. Communities are constructed with no plan for where people living in the community will shop or send their children to school.

For economic purposes, it is the infrastructure of roads and rails that needs to be massively built up. Paved roads can only get you to a handful of places in the country as the majority of the world’s 19th largest country is connected by dirt roads (#18 is Iran and #20 is Peru). The different levels of efficiency between transporting coal, copper, and other natural resources by rail compared to trucking out product on dirt roads is huge.

The government has proposed a 3-phase plan to develop the rail system, and have discussed making an IPO of Mongolian Railways as early as next year to help fund the rail network’s development. A major problem in developing the Mongolian Railways is a holdover from the communist era: Russia owns 50% of Mongolian Railways. Thus, Russia can block any development of the Mongolian rail system of which it does not approve. The government would be wiser to allow for private companies – including the mining companies – to develop the rail network privately and separately to scale up the rail system to meet their export needs. There has been concern in the government that allowing private rail systems to be built will lead to a myriad of umbilical cords to China. The government could set up a credit bank – similar to a carbon tax system or the Everglades Bank model in Florida – that would cause private companies building their own rail networks to China to have to put a certain amount of funds in a sovereign Mongolian credit bank that built an equal amount of rail network toward Russia, Kazakhstan, India, and Korea. However, concerns about being over-reliant on China have trumped coming up with innovative ideas to develop the rail system more rapidly.

Change in government policy toward business and investors

Everyone I spoke with in Mongolia believes the government is stable and will continue to support the country’s economic development regardless of whether Mongolia’s Democrat Party or Mongolia People’s Party wins the elections next year. This was true even of people working for government and non-government organizations that did not particularly like everything happening under the country’s current trajectory.

Yet, in September 7, 2011, a group of 20 Mongolian lawmakers sought to change the Oyu Tolgoi agreement from the government having a 34% stake in the mine to a 50% stake in the mine. This seemed to be election-year posturing in a democracy, with elections slated for next June. The damage of changing this agreement would be similar to the economic damage of the Windfall Profits Tax of 2006, and the analysis of Mongolian-based investment professionals is that it is impossible that something so foolish would be done again. Multiple media outlets misrepresented the action of 20 members of a 76 member parliament as an action of the "Mongolian government" which caused Ivanhoe's stock price to tank precipitously. In the end, the government came out and made a joint statement with Ivanhoe and Rio Tinto that the agreement would not change, and Ivanhoe's share price has subsequently recovered. Oyu Tolgoi, along with Tavan Tolgoi, are the centerpieces of a mining boom expected to keep GDP growth well above 10% for two decades or more.

In any country, including your home country, there is always the risk of changes in laws impacting your investments whether they be tax laws, property laws, mining laws, trading regulations, or other changes. Two people I met who are both against government policies and work for governmental agencies both believe the government, and government policies, will be stable, regardless of election results. The two large parties, the MPP and the Democrats, are viewed to be of like minds on economic policies. This belief is in large part based on the fact that most of the people in the government are related to people profiting from business in Mongolia, or are directly profiting from Mongolia’s business development themselves.

Disclosure: I am long Mongolia Growth Group, Origo Partners, and Ivanhoe Mines. I have made no trades or investments in the above listed investments in the week preceding publication of this article and will make no trades in any of the above listed investments in the week after this article’s publication.

No comments:

Post a Comment